How to Save Money, No Matter What Your Age

Financial experts show you how to save money and get your investments in order this 2024.

New year, new you, and what better way to improve than to start with your finances? We spoke to the experts Astro del Castillo, President of First Grade Holdings Inc., and Helen Oleta, Vice-President of the Fund Managers’ Association of the Philippines (FMAP) for tips on how to save money, no matter how old you are. Their advice can help you learn how to get your finances in order this 2024.

The 50-30-20 method

Any method that teaches how to save money starts with following a budget. One such method is the tried-and-tested 50-30-20 method. The idea behind the method is to spend 50% of your income for bills, needs and other obligations (rent/mortgage, utilities, grocery, etc.), 30% for everything else you might want (dining out, shopping, gym membership, etc.) and 20% for saving and investing.

A variation of the 50-30-20 method is the 40-30-20-10 method. Here, a smaller percentage of 40% is allotted for necessities and the rest remains the same, but in addition, 10% is allotted for charity or church donation.

40% – bills/necessities

30% – wants

20% – savings or debt repayment

10% – charity

Investment Stages

Now that you know how to divide your income, you can decide how to invest the excess. Your investment decision will depend mainly on two things: Your risk appetite and you age. For Astro del Castillo, President of Fund Management Company, First Grade Holdings Inc., a simple guide is to divide investors into three main categories:

20-39 years old – Higher tolerance for risk, with a longer investment horizon

40-50 years old – Moderate risk, with an increase in fixed income investments

51-59 years old – Less risk, with a focus on capital preservation

60 years and above – Retired or semi-retired and living on interest

How to Save Money in Your 20s to 30s

The 20s to 30s is a time of learning. Maybe you’ve just started to earn your own money, and want to reward yourself by travelling. But before you do, know that this period of your life is a good time to start saving and learning about various investment options as well.

Del Castillo explains that since you are still decades away from retirement, you still have time to learn, take risks, and even make some mistakes. “Young investors have a longer investment horizon and a higher tolerance for risk, and higher risk, means potential for higher returns.”

Del Castillo recommends investing 30% to 40% in stocks, 20% to 30% in real estate, and 40% to 50% in low-risk, fixed income investments such as government and corporate bonds, and Pag-ibig MP2.

Most of these investments are easy to make. You may inquire with your bank about bond investments and mutual funds that invest in fixed income investments (bonds, treasury bills, time deposits).

Pag-ibig MP2, meanwhile, currently offers one of the highest rates in the market at 6% to 7% annually. But while the rates are attractive, you will need to park your funds with them for five years, and be an active Pag-ibig member. In case you’ve been delinquent, just resume your contribution as voluntary or self-employed, and a single contribution will already allow you to open your MP2 account.

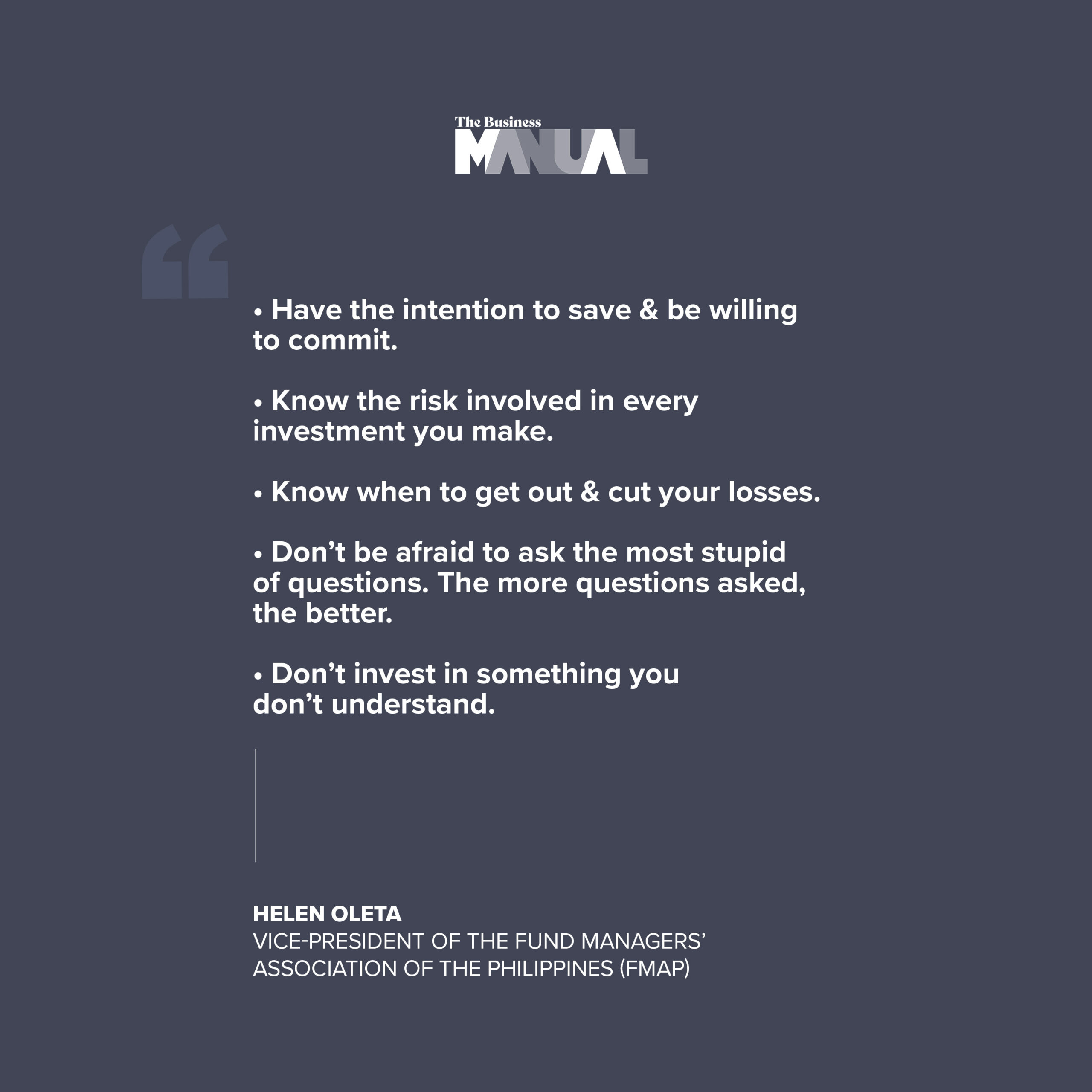

Helen Oleta, Vice-President of the Fund Managers’ Association of the Philippines (FMAP) on the other hand, prefers to stick with government securities (government bonds, bills, and notes). She explains that unlike other fixed-income investments that require you to park your money for a number of years, government securities can be easily traded in the secondary market anytime. “It’s a tradeable asset. You can sell it anytime you want,” she says.

Oleta adds that now may be an opportune time to invest in fixed income funds before interest rates decline. “We’ve seen the peak of inflation, but the rate is still high at this time. Central banks globally will reduce rates in the next one and a half to two years because of easing inflation,” she says.

When it comes to stocks or equities, Oleta recommends putting most of your money on blue chips and index stocks that have a stable track record and financial performance.

Del Castillo agrees, and vouches for blue chips such as Ayala Corporation, Meralco, PLDT, San Miguel and the like, that are stable and offer dividends. “Stocks beat inflation and other investment instruments in the long term,” he says. “But choose the blue chips and companies that give out dividends [such as] the Ayalas, Sys’ holding companies, banks, and utilities,” he adds.

If you’d like to consider US and other foreign stocks, fund managers recommend starting by investing in a local equity fund that invests abroad, rather than investing directly, in order to be better protected.

Once you have formed a considerable amount of savings, you may also look into real estate investment and utilize your benefits under the Pag-ibig Fund. The government agency is known to offer lower rates over a longer payment period.

Ideally, the rental income earned from the purchased property, should be able to cover your monthly amortization.

How to Save Money in Your 40s

Your 40s is a time for reducing risk and saving more for your retirement. You still have a moderate risk appetite and still invest in stocks, but choose more blue chips and strong second-line stocks, while reducing speculative investments. If you started investing in real estate in your 20s, you would be finished paying your mortgage during this period.

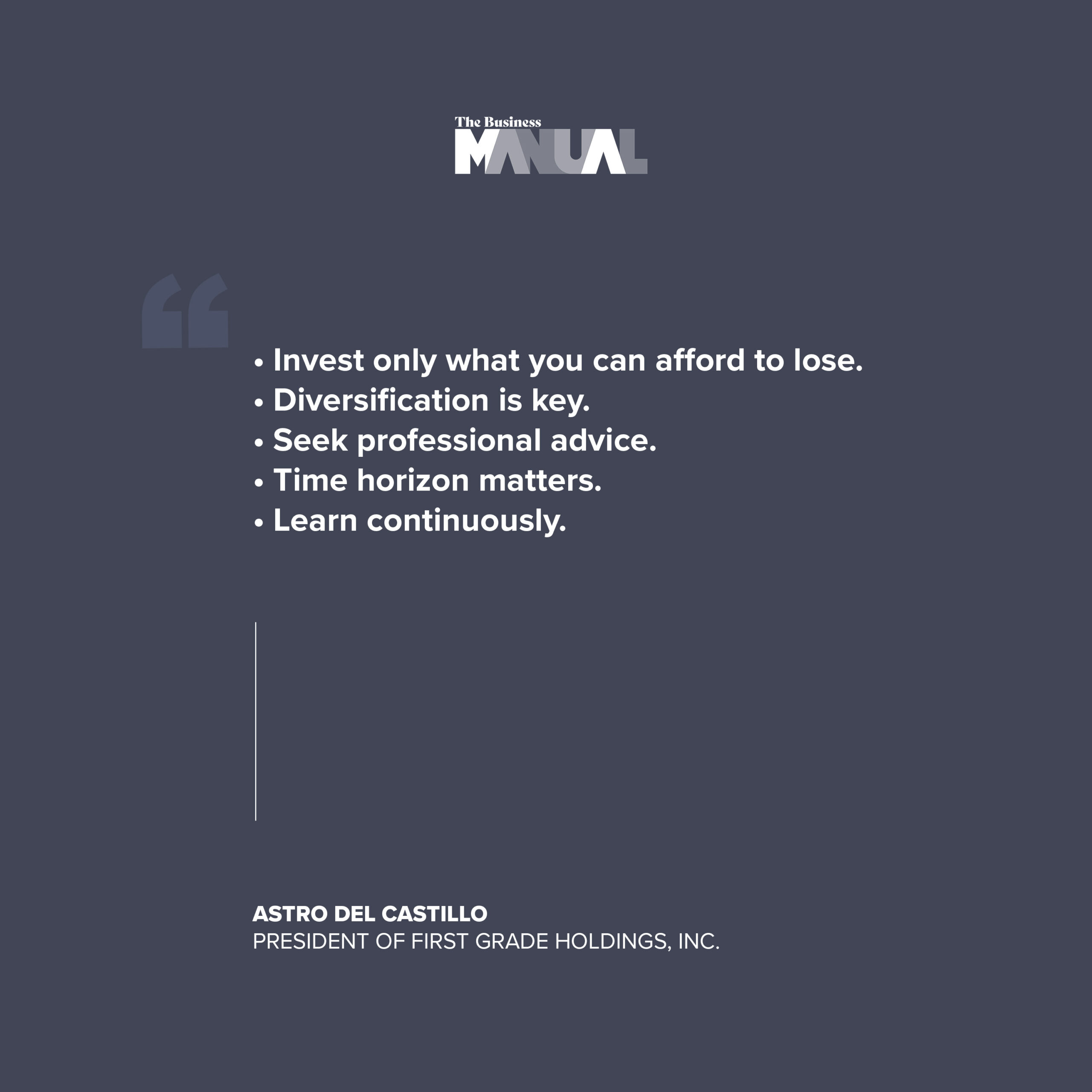

“Invest only what you can afford to lose,” del Castillo advises. This serves as his guiding principle, in calculating his personal risks and investment decisions. If the money to be invested is an amount you cannot afford to give away, he warns clients against doing so, regardless of how tempting the potential return may seem to be.

How to Save Money in Your 50s

At this stage in your life, you need to begin preserving your capital in preparation for retirement. Majority of investments will be in low-risk, fixed income investments. You may still invest in higher-risk assets but lessen it to just 20% to 40%, depending on your risk appetite and what you can afford to lose. With only a decade left before retirement, it is ideal to have established several passive income streams such as interest income and rental revenues.

How to Save Money in Your 60s

You have prepared for your retirement and can now live on interest, and other passive income sources.

It is important to remember that these investment stages merely serve as a general guideline for how to save money. They should not put added pressure on your shoulders. Income, investment losses, and certain life events may affect how much you earn and save in various stages of your life, and that is okay. “Save early to develop the discipline, but also remember to enjoy life,” reminds Oleta.

Case Study: Tara’s Investment Journey

Tara, not her real name, started investing in her mid-20s. Working in a government housing agency, her initial investment was in properties, particularly low-cost government housing projects. Gradually, she also learned about other investment options from her bank, and began investing in bonds and other fixed income instruments.

“Being a family breadwinner, and then later on, a single mother with three kids, I was very diligent about saving,” Tara recalls. “I took advantage of investment opportunities in my work and always spoke with my bank about other investments aside from the regular savings account.”

She considered herself a conservative investor and generally avoided riskier investments. “My greatest fear then was if someone got sick or if there was a major emergency and I didn’t have enough cash on hand. So I made sure I was liquid, and had a separate emergency fund,” she shares.

Today at 75 years old, with three grown children, Tara says she is generally satisfied with her investment decisions. Her real estate investments eventually expanded to include more prime properties, whose values have doubled and tripled, and are now generating rental income. “Always invest on land (instead of condos), because that appreciates,” she advises.

Is there anything Tara would have done differently? “Maybe make more real estate investments in good locations,” shares Tara. “I also regret not being able to diligently watch all my investments and not having more time to study (personal finance).”

Tara recalls the worst investment she made was in a popular education plan. The fund eventually went bankrupt and closed in the 90s, with her, and thousands of others, unable to recover their investment.

Learning from that experience, she warns that you have to be discriminating with who you invest with. These days, scams are rampant and many investment companies just suddenly close and disappear. “You have to do your research and know the company’s background. Be meticulous,” she cautions.

Latest Cover

Let TBM’s fact-based journalism help you gain curated knowledge and stories straight from the professionals.