Blockchain 101: Different Types, Pros, Cons, and Practical Uses

Blockchain technology is known for its practical applications in various businesses and industries. We delve into the different types and their uses.

When Bitcoin was created in 2008, blockchain technology emerged as the backbone of what made it a peer-to-peer network—defined as partitioning tasks or workloads between peers. By then, it was only recognized as the distributed ledger behind Bitcoin transactions. However, in 2014, blockchain separated from Bitcoin, as its potential beyond being a currency was explored.

Since then, blockchain has grown to be more than just a distributed ledger for cryptocurrencies. In fact, it has also been integrated into various industries outside of finance. This is because this technology can be used to make any data in any industry immutable or impossible to alter.

As of 2023, there are over 1,000 blockchains used across the world that cater to a wide range of industries. This was made possible by the fact that there are four blockchain types that make it applicable for various uses.

In this article, we define them and determine their pros, cons, and practical uses.

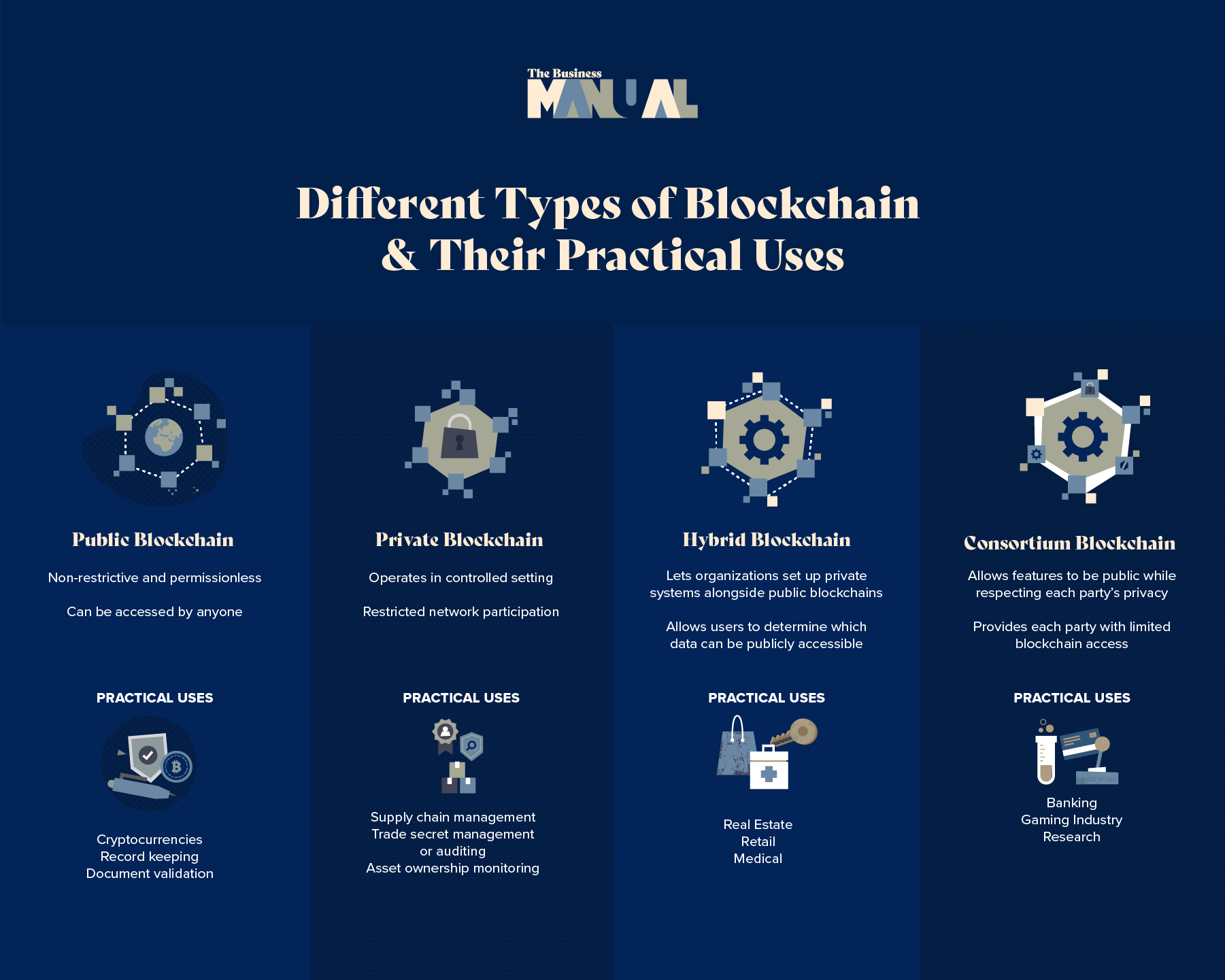

Public Blockchain

A public blockchain is characterized by being non-restrictive and permissionless. As a result, anyone with internet access can use the blockchain platform, become a trusted node, and join the network.

Among the many things that public blockchain users can do include viewing both recent and old data, confirming transactions, and mining new blocks—defined as “the process of adding transaction records to the bitcoin blockchain.” Aside from those, public blockchain also has two main uses: currency mining and exchange. When it comes to transaction verification, this is done effectively with the help of consensus methods like Proof-of-Work (PoW) and Proof-of-Stake (PoS).

Popular examples of public blockchains include cryptocurrencies such as Bitcoin, Ethereum, and Litecoin.

Practical Uses:

- Record keeping

- Document validation

- Affidavits and public records notarization

Pros:

- Requires no intermediaries

- Remains completely independent from organizations

- Ensures network transparency

Cons:

- Can be slow

- Usually doesn’t scale well

- Security may depend on how users follow safety protocols

Private Blockchain

Unlike public blockchains, private blockchains operate in a controlled setting, given that these run under closed networks. These are frequently used within organizations where network participation is restricted to a chosen group of people. This is why these are often known as enterprise blockchains or permissioned blockchains.

They resemble public blockchains in some ways because they also use peer-to-peer connections, while being decentralized, meaning that all users collectively retain control. However, they are only used in constrained and small networks. Being private also means that specific organizations have control over security settings, permissions, and accessibility.

There are several private blockchains today but some of the most recognizable ones include IBM Blockchain, SoluLab, Tech Alchemy, and Cubix.

Practical Uses:

- Supply chain management

- Trade secret management or auditing

- Asset ownership monitoring

Pros:

- Faster transactions

- Better scalability

- Ability to deny third-party access

Cons:

- Limited transparency

- Possible governance issues

- Lack of trust (since external users will have no control over the verification of their transactions)

Hybrid Blockchain

Hybrid blockchains are known for combining the principles of both public and private blockchains. This allows organizations to set up a private system alongside a public blockchain. Therefore, users can manage who has access to particular data recorded in the blockchain. They can also decide which data is accessible to the general public.

Hybrid blockchain transactions are typically private but can be viewed using smart contracts—defined as “a self-executing computer program that automatically executes the terms of a contract without the involvement of third parties.” Even though the information may be private, the network remains verifiable. This blockchain technology also enables private firms to own the blockchain and prevent them from making changes to it. However, users’ identities are kept private unless they conduct transactions.

Popular examples of this are XinFin, IBM Hybrid Blockchain, and Quorum.

Practical Uses:

- Real estate

- Retail

- Medical (for safekeeping medical records)

Pros:

- Not accessible to hackers

- Protects privacy while still allowing communication

- Cheap and fast transactions

Cons:

- Not fully transparent

- Can be hard to upgrade

- No incentives for network participation and contribution

Consortium Blockchain

Consortium blockchain sets itself apart from the aforementioned types of blockchain. This is because it works as a creative approach to solving needs that may require both features from public and private blockchains. Here, some features can be kept public, while the privacy of the other aspects is preserved.

What sets this apart from the rest is that it allows several organizations to collaborate on making this decentralized network work. More so, each party can only enjoy limited blockchain access, thus removing the risk of letting one party have more control than the others.

Some of the most recognized consortium blockchains are Hyperledger, Ethermint, and Multichain.

Practical Uses:

- Banking

- Gaming industry

- Research

Pros:

- Enhanced security and scalability

- Smooth access controls

- Better data privacy

Cons:

- Less transparency

- Less anonymity

- Risks of having a conflict of interest

These are just the four blockchain types that people use today. By understanding these and seeing beyond their connection to cryptocurrencies, people can be more open to learning more about this and what it can be used for.

And since several countries are becoming open to this new technology, it may be sooner when people get faced with the uses of blockchain technology without seeing it as a complicated concept to grasp.

Latest Cover

Let TBM’s fact-based journalism help you gain curated knowledge and stories straight from the professionals.